Earnings Wrap

Earnings Wrap

Madison Square Garden Ent. & Gamehost

One prospective and one held company have reported quarterly earnings, lets take a look.

Madison Square Garden Entertainment Q3 Earnings Report ($MSGE)

FY24 Revenue Range Narrowed to $940-950 Million, as Compared to Prior Range of $930-950 Million

FY24 Operating Income Range Increased to $100-110 Million, Versus Prior $95-105 Million

FY24 AOI Range Increased to $200-210 Million, as Compared to $195-205 Million Previously (1)

Christmas Spectacular: Revenues Increased 13%, shows Increase 7%, demand remains strong for next season

Revenues & Operating Performance

Revenues grew to $228.3 for the quarter and increase of 13%, with revenues increasing 10% financial year-to-date.

Increased revenues were primarily due to increased event-related revenues with both Knicks and Rangers into their respective finals series.

Decreases in both Operating income (-32%) and Adjusted Operating Income (-23%) as higher costs eroded profitability during the quarter.

Direct operating expenses increased by 25% against the prior quarter, this was a result of an increased number of events, and higher per-event costs

SG&A was 23% of revenues for the quarter and was within the mid-point for historical averages, however, this was a 22% increase on the prior year as all associated costs were not yet felt in FY23 due to the spin-off.

AOI as a % of revenues was 16.5%, at the mid-point for historical averages, whoever, there is some volatility, with the Christmas quarter driving 75% of yearly operating income.

Business is still working through Sphere related expenses and restructuring charges

Financials

Interest expense remains elevated as the company holds significant debt - 6.7% of revenues.

Management are not looking to significantly reduce debt and rather see the business naturally deleveraging as Adjusted Operating Income increases in coming years.

SBC for the quarter was $5.6m, and is forecast for $28m for FY24, worth noting the company since the spin-off has returned $140m through buy-backs and has $110 remaining in the current facility.

Net debt stands at $602m and is approximately 3x leverage.

Notes from Earnings Call

The increase in AOI by $25m is largely the result of an accounting change, where non-cash revenues from the MSGS agreement will now be factored into AOI moving forward, so no real excitement there, although it was revised up by $5m.

Christmas Spectacular demand remains strong across all segments;

Christmas Spectacular sales, whilst early in the year are up approximately 35% on the prior year. Management believes there is optionality to increase pricing, events and ticket yield, which are all very margin accretive.

Dynamic pricing and the spectaculars discount to alternative Broadway shows leave it will positioned for continued growth.

Continued suite and hospitality demand at MSG

You may recall from my initial note, management recently introduce new suites and a bar in the hospitality section. Both have been incredibly well received, and management is now exploring additional capacity to meet demand.

Driving hospitality directly effects profitability as management squeeze more juice out of current capacity.

Margin Expansion remains the focus

As discussed previously, venue utilization, further hospitality offerings, dynamic pricing, decreasing venue changes through longer performance schedules are all ways management are looking to drive profitability.

Management is not seeing the consumer weakness that McDonalds & Starbucks are.

Summary

This was a mixed quarter for MSGE, while the business continues to perform well, with all key venues forecasting continued strong demand, management now has the freedom & opportunity to explore different ways to drive optimization and leverage within the business. (We have seen this with the introduction of dynamic pricing & Oaktree taking over sponsorships)

However, MSGE remains a cost-intensive operation, and management will need to find ways to optimize operations to improve profitability in the face of rising costs.

Peripheral costs from the spin-off are still impacting cash flow and profitability on a look-through basis, meaning the true economics of the business remain somewhat obscured. Nevertheless, the premium assets and brands under the company's control, coupled with the ongoing strength of the consumer, position MSGE to be a cash-generative compounding machine for the long term.

In the short term, the share price may have deviated from the fundamentals, and with a likely slowdown in the retail space, it wouldn't be surprising to see MSGE decline over the coming quarter. I've taken today's price movement as an opportunity to initiate a position and will consider adding more depending on price action.

At 20 times EBIT and 10 times AOI, MSGE is still trading on the expensive side.

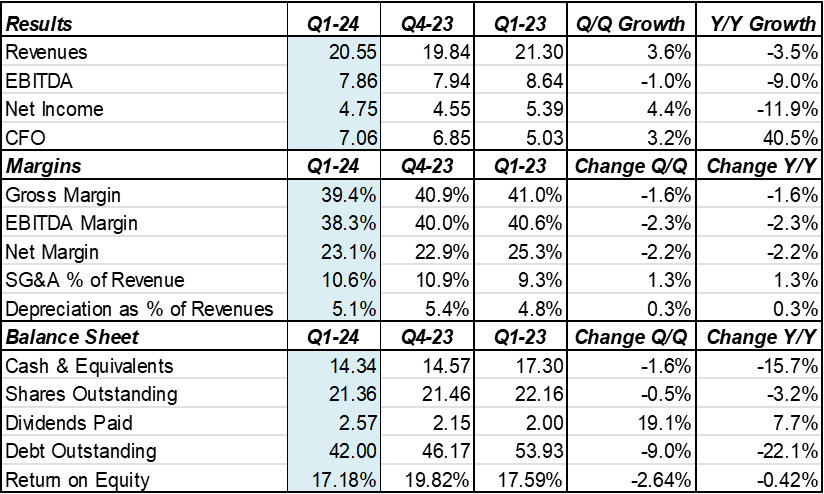

Gamehost Q1 Earnings Report ($GH)

Gamehost operates a variety of gaming, hotel and entertainment venues in Alberta, Canada.

Revenues & Operating Performance

Please note this quarters results were influenced by a period of record-breaking cold in mid-January.

Revenues increased by 3.6% through the first quarter, although they declined year over year.

EBITDA and operating cash flows remained strong but slowed on yearly comparisons as high interest rates began to influence consumer activity and higher costs weighed on margins.

Room revenues experienced a 6% year-over-year decline, with occupancy rates dropping from 63% to 59%. However, Average Daily Rates remained stable.

Gaming revenues increase 7.5% YoY, with margins increasing from 59% to 61%

F&B revenues declined 3.6% YoY

Management made note of a softening consumer during the prior quarters MD&A, a period of extended cold in January alongside interest rates pressures may see some weakness in the short term.

Financial Performance:

Cost of Sales increase to 60.6% from 59.1%

Operating labor costs continued to rise, increasing from 27.5% to 29%. Management attributed this increase to staffing levels not being optimal for the decrease in consumer activity caused by the January cold snap.

Margins experienced a mild decline across the board, with a slight uptick in costs of SG&A and Depreciation.

Furthermore, marketing costs increased to 5.3% of revenues from 4.4%, as Deerfoot Casino invested in promotions to support high limit gaming.

Dividend and Share Buybacks:

Gamehost remained committed to returning capital to shareholders, repurchasing 48,200 shares at an average price of $9.65. The pace of buybacks slowed this quarter, possibly due to the increase in the Gamehost share price or as a result of the 2% tax on buybacks implemented by the House of Commons.

Gamehost paid 12c per share in dividends through the 1st quarter.

Gamehost retired $4.2m in debt outstanding, reducing the total to $42m.

Commentary from Management

Gamehost management acknowledged the impact of adverse weather during the quarter but maintained optimism regarding the overall health of the Alberta area. They observed some softening in consumer behavior, which has been noted. However, with warmer weather approaching, an uptick in activity is anticipated in the coming months

Management also made note of the Trans Mountain Pipeline, the pipeline once plagued by delays is now under commercial service as of May. The benefits of the pipeline are expected to spill over to every Albertan’s and continue to lift activity along side increased migration to the area.

Summary

Gamehost is up 8% year to date and continues with its no-frills performance. Management demonstrates a deep understanding of their business and the economic landscape of Alberta. I remain excited to see them deliver on their goals of maintaining a stable dividend, repurchasing shares, and, once debt levels have been reduced, investing in growth.