New Position: Chorus Aviation

New Position: Chorus Aviation

Undervalued, under covered and catalysts ahead.

I have opened a new position in Chorus Aviation (TSX) and wanted to share a quick thesis whilst the stocks trades near the same price point. (Purchased at $2.19). I have not had the time to conduct the equivalent level of research as previous posts, however, I feel the Chorus value proposition is quickly turning and we could see the stock move in the near term.

*Please note this idea was shared first on MicroCapClub by “AgentSmith”, and after researching the past fortnight, I believe it is an asymmetric opportunity and have decided to open a position*

*All values in CAD*

Ticker: Chorus Aviation (CHR)

Index: TSX

Market Cap: $448m

EV: $1.98B

S/O: 196m

EV/EBITDA NTM: 5.1x

1. Who is Chorus Aviation?

Chorus is a global aviation solutions provider and asset manager, focused on regional aviation. It operates three key segments.

Jazz Aviation - The largest regional airline in Canada and provides regional air services under the Air Canada express brand.

Falko - A leading regional aircraft asset manager and lessor.

Voyageur - A leading provider of specialty charters, aircraft support, maintenance and modifications and parts provisioning .

Through these subsidiaries Chorus is involved in every stage of the regional aircraft’s life cycle.

2. Background

In 2021, Chorus undertook steps to transition it’s business from regional airline operations to an asset-light airplane leasing model, which was achieved through the acquisition of Falko, a leading pure-play regional aircraft asset manager and lessor.

The business model transition has been slower than expected and this has seen the stock’s performance lag peers. With significant leverage from both it’s regional airline Jazz and the acquisition of Falko, financing costs have weighed on Chorus earnings.

Fast forward to today, I believe sentiment has shifted and Chorus is now positioned to benefit from renewed interest. The company is seeing return on it’s investment in Falko as the business generates significant cash flow. This has allowed Chorus to reduce leverage substantially reaching the upper band of their leverage target. I believe this will provide ample opportunity for management to re-focus on business growth and increase the pace of capital return.

Finally, regional airlines remain a vital cog in the global economy and play an essential role in connecting communities to key airports. Post-covid the regional airline leasing landscape has seen a plethora of changes leaving only a handful of operators in the market.

3. Thesis

I see this position playing out as a medium-term hold with limited downside risk. Chorus is in the final stages of it’s company transformation and the investment is highlighted by the below.

Over $1 billion in future contracted lease revenues - Stable cash flow source from CPA and contracted agreements.

Trading at a fraction of it’s book value - Falko is actively transacting in owned aircraft’s where feasible and returning capital to the business to both de-lever and repurchase shares.

Increasing margins - Improving margin profile as leasing revenue makes up a greater portion of revenue.

Achieved target leverage - Lower interest payments will increase earnings, flexibility to invest in growth and return capital

Increasing free cash flow - The move to asset-light model will continue to improve the companies ability to generate free cash flow (FCF has increased 35% over last 3 years)

Tailwinds in the industry - Forecast $650B in investment required to replace ageing aircraft fleet by 2040.

I believe we could also see the below catalysts occur to trigger a share price re-rating.

Reinstatement of a dividend - management has expressed interest

Share repurchase activity - Chorus has repurchased 5% of shares since 2022. Management is actively repurchasing in the low $2 range, providing a floor on the share price.

Close of Falko Fund III - Falko is expecting to close it’s third investment fund this year which will provide additional revenue and investment opportunity.

Retirement of Preferred Shares - which are diluting the true earnings power of Chorus subsidiaries.

4. Strategy

Regional aviation as an industry has proved to be incredibly resilient, as it stands approximately 45% of all airports are served exclusively by regional aircraft’s. With a reduction in operators and aircraft leasing services since covid, this provides ample room for growth in Chorus key segments.

Chorus intends to continue it’s transition to an asset-light model. What does this mean? Chorus will lean on the expertise of Falko in aviation asset management to invest, lease and operate regional aircraft’s using third-party equity, rather than it’s own capital, reducing stress and leverage on the balance sheet.

Chorus’ strategy for its leasing business is to:

Transition to a less capital intensive approach to growing the regional aircraft leasing business;

Generate higher quality cash flow streams in the form of asset management fees;

Reduce leverage and balance sheet risk, thereby improving cash flow generation; and

Enable Chorus to better serve the needs of its leasing customers by deploying larger tranches of equity capital alongside third-party fund investors.

Targeting mid-teens IRR

Investing in Growth

Grow core services, focus on recurring long term contract cash flows - Jazz & Voyageur

Grow recurring asset management fees from aircraft investment funds - Successor funds and new strategies - Falko Funds I, II, III

Recycle capital to common shareholders and or reinvest in acquisitions - Bolt-on

5. Business Segments

Chorus services both business and government through each of it’s underlying subsidiaries with a focus on long-term contracts to ensure stability in cash flow. Company subsidiaries are split into two key segments.

Regional Aircraft Services

Jazz - The largest regional operator in Canada and provider of regional air services under the Air Canada Express brand.

Jazz is the main Air Canada Express Operator

Fixed Fee defined until 2035

Lease income from aircraft’s

Incentives related to operational performance

Voyageur - A leading provider of specialty charter, aircraft modifications, parts provisioning and in-service support services.

A leading provider in specialist aviation

Demonstrating exceptional growth with a 35% target by 2025

Growing defense sector contracts in parts provisioning and sales, and engineering and maintenance.

Regional Leasing Services

Falko - The leading pure play regional aircraft asset manager and lessor, managing investments on behalf of third-party fund investors.

Excellent management team with over three decades in experience and an extended history of generating mid-teens IRR.

200* aircraft’s under management, utilized by over 40 global airline customers.

Generates revenues through asset management fees, performance fees in-line with funds & realized gains on asset sales.

Chorus has realized substantial gains on aircraft sales in recent quarters, this could provide additional upside to debt reduction & capital return.

Management believe the market opportunity at this time, is the best they have seen in decades.

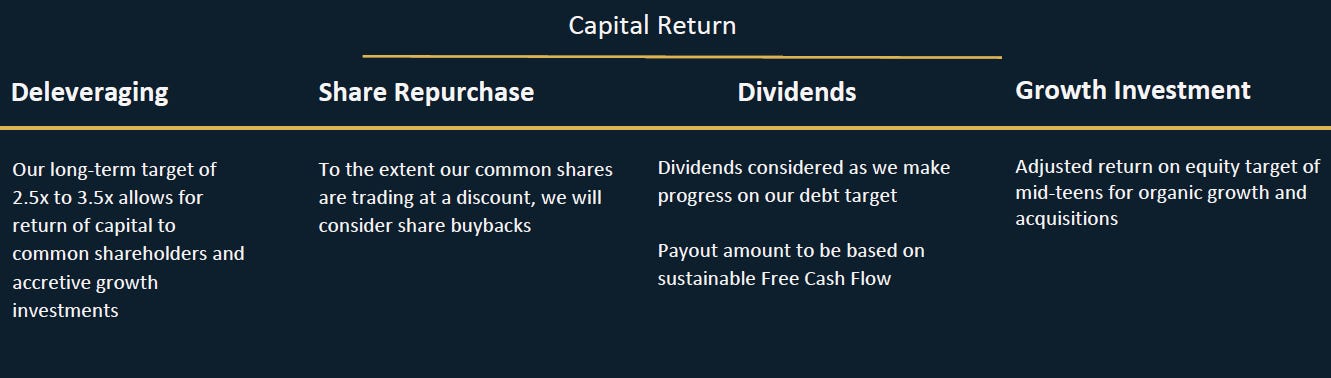

6. Capital Allocation

Management is looking to continue growing the asset management and leasing arm of the business, including the inception of Falko Fund III. Alongside the fixed revenue sourced from Jazz and the faster-growing Voyageur the company has developed a stable base of cash flows that can allow the company to continue to realize capital allocation goals of: (in no specific order)

Reducing debt

Growing Falko & Voyageur

Repurchasing shares

Reinstatement of dividend

It is also worth highlighting the related parties involved with Chorus Aviation, Air Canada maintains a board seat and equity ownership, but more specifically Brookfield Asset Management. To secure the financing for the Falko transaction Chorus engaged Brookfield AM, who currently hold 13.2% at a cost base of $3.79, significantly below the current price. The company also holds 300,000 preferred shares at 8.75%. At the current rate, the preferred dividend payments are consuming a large share of the net income available to common holders. I personally would prefer to see management repurchase the preferred shares, which they have the option. As at the end of 2023, management believed the repayment of debt and repurchase of shares served as a greater return on capital. Moving towards the mid-point of the year, with leverage quickly reaching target levels, I would be looking for management to consider retiring the shares.

7. Risks & Competition

With significant portion of revenues tied to long term contracts and the inherent value in the underlying assets of Chorus, I believe downside risk to be limited. Chorus interacts with global and in most cases large-scale aviation operators providing the company stability. Some counter party risk does exist, however, in certain cases regarding receivables we have seen Chorus work with counter parties to ensure delivery of outstanding payments, whether through restructuring or alike.

Aviation has historically faced difficulties in demand cyclicality and poor returns on capital, Chorus’s movement to an asset-light model will reduce reliance on conventional revenue streams in the aviation industry.

A concern of mine regards management incentives. Whilst management has been executing extremely well since company transformation, there remains a lack of insider ownership from management. Management has highlighted their disappointment in the share price and expressed their desire to improve this through a variety of initiatives including capital return. I would like to see management investing alongside the common holders and purchasing on-market, re-enforcing their claims that the share price is indeed extensively undervalued.

A note on competition, Jazz’s fleet is significantly larger than that of the next largest Canadian regional airline. All other carriers in the Canadian regional airline market are smaller operators of turboprop and regional jet aircraft. Therefore, Jazz gains a competitive advantage from its scale of operations, and access to and ability to train pilots and other human resources at scale.

Falko is currently the leading lessor and asset manager focused solely on the regional aircraft segment due to the size of the fleet it manages and the breadth of its relationships with capital providers. Whilst there are other operators in the space, management’s 30 year history position them well within the market and provide them with an edge in transactions.

8. Financials & Valuation

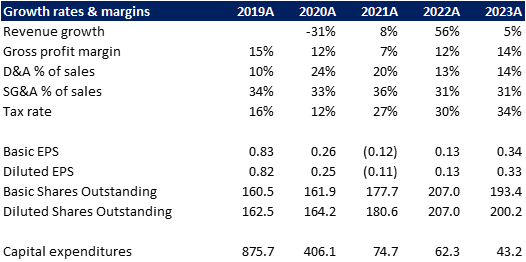

Revenues have increased since the acquisition of Falko. However, moving into 2024, revenues and EBITDA are both expected to decline. This is largely due to two factors:

The revised CPA agreement with Air Canada will result in lower revenues moving forward as the number of aircraft declines, aligning with the company's asset-light strategy.

Fixed margins and other revenues associated with the CPA aircraft will also decrease over time as the aircraft’s age.

Regarding the associated debt with each aircraft, as the debt servicing for each corresponding aircraft is reduced or extinguished, each aircraft lease can be renewed or entered into a new lease at significantly higher margins as the need for interest payments subsides, supporting higher earnings.

Highlighting capital expenditures, we can see the companies asset-light strategy in place as expenditure declines year over year. This is the effect of management utilizing Falko, and third-party resources, to contract in aircraft’s without the need for significant capital outlay. This increased flexibility will allow management to be more targeted in their segment growth.

Finally, I am looking for improved margins as a greater percentage of revenues is contributed from RAL as compared to the op-ex heavy RAS segments.

In terms of valuation, as always I believe any forward looking estimate should be taken with a pinch of salt as assumptions can shift at any time. However, using base line assumptions in revenue growth, margins and capex requirements we can see the company appears significantly undervalued, even after applying a margin of safety.

As highlighted I believe there are near-term catalysts that could see momentum lift the Chorus share price, including most recently the Bank of Canada beginning it’s rate cutting cycle.

That’s all folks,

I hope you enjoyed this write-up and consider investing in Chorus Aviation.

Disclosure: I hold a position on Chorus Aviation, first purchase was on the 28th of May at a purchase price of $2.19. This blog is merely to document investment ideas and commentary and it is not meant to be financial advice. Please conduct your own research on all investment