Quick Idea: lululemon athletica

Quick Idea: lululemon athletica

Quality at a discount!

Going to keep this fairly short, as I have not had the time to perform a more thorough due diligence and want to provide the opportunity before any potential market movements.

lululemon athletica Investment Thesis

Premium brand

Loyal consumer base

Rapid growth of Membership Program, reaching 17 million in just one year

Demonstrated management quality and effective execution

High margins, strong cash flows, repurchasing shares

Competitive space, gaining market share and large, growing TAM

Significant opportunities in product growth

Why does the opportunity exist?

After disappointing lofty analyst expectations in the Q4 Earnings report and guiding to lower revenues and a slightly weaker consumer in the US, LULU 0.00%↑ has sold off significantly over the quarter and trades today at a forward P/E of 25x against a 10 year historical average of 43x.

Management has assumed blame for inventory constraints this past quarter and has commented on resolving this heading into the remainder of the year. With the US consumer remaining resilient, and economic conditions easing, I expect Lulumemon will beat on earnings throughout the year and revert back to historical multiple levels, paving the way for a solid return.

Let’s see if there is an opportunity here.

Company Overview

Lululemon is a leading premium apparel brand in Canada and North America, has compounding revenue growth for over two decades. Originating in the yoga space, it has since diversified its offerings extensively and now encompasses a wide array of apparel, including clothing for both men and women, along with accessories and footwear.

The company prides itself on providing high quality apparel and accessories to a diverse user base and leverages it’s ability to innovate in the fabric space to command pricing premiums. What does this mean? The quality of the items is extremely high, Lulu boasts quality fabric innovations such as Luon and Nulu, which target moisture-wicking and stretch and breathing properties, and so this means the retail costs can be eye-catching.

A key bear thesis for Lulu has been whether or not the company exhibits ‘Fad’ characteristics, however, successfully expanding it’s product categories and being able to continuously drive demand over an extended period of time, I believe speaks to the strength of the business and it’s staying power.

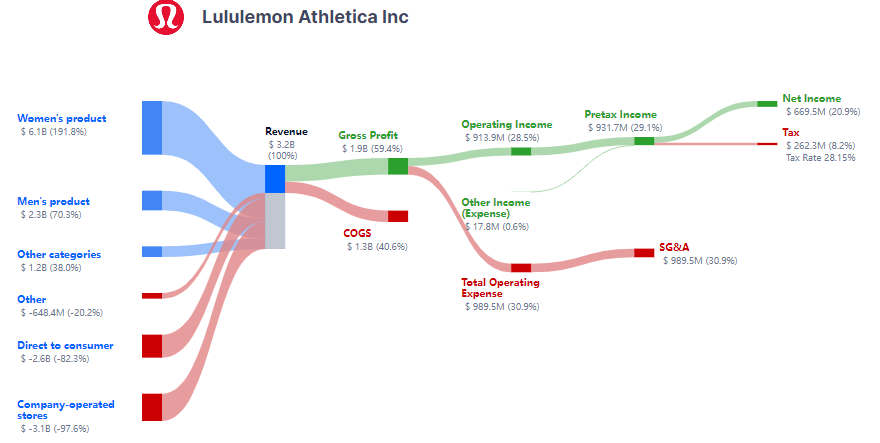

How does the business generate revenue?

The majority of revenue is earned through women’s product channels, over decades Lulu has built up trusted brand recognition with it’s female consumers and has expanded beyond Yoga, to training, gym and casual apparel. Female consumers often purchase discretionary items in much greater frequency than men, and exhibit greater brand loyalty. Lulu has also been expanding into the Men’s category with clothing and more recently Lulu’s Men’s training shoe.

Americas makes up over 80% of revenues with China and the Rest of World sharing approximately 10% each. This leaves a large potential market for expansion which should see revenue growing mid-teens for years to come.

Locations have exploded over the past 5 years growing from 500 to over 700 today. Lulu has expressed it’s desire to increase locations this year, with 5-10 stores planned for the US, additional optimizations also, and potentially 30-40 stores in China where it sees runway for growth.

Growth Opportunities

Geographical Expansion

As highlighted, the majority of revenue for Lululemon is being driven out of the Americas, with a growing middle class globally, there is ample opportunity for expansion over the coming decade. International revenues grew 54% in Q4 and this trend should continue for some time, as management can lean into a strong balance sheet to drive growth.

Product development

By engaging consumers through a community feel, Lulu has been to leverage it’s brand loyalty to capture the consumer in a variety of ways. Expanding their product arsenal to capture both athletic and casual apparel needs, means the company is becoming part of the consumers entire day, not just a couple hours of it.

Beyond casual wear, Lulu has expanded into direct sporting attire and accessories, most recently footwear and Men’s golfing apparel. Early signs are both appear highly popular.

Membership Growth

Lululemon implemented it’s Essentials membership program just over a year ago and to date has over 17 millions members. This demonstrates the brands strength and loyalty and should create a flywheel effect for sales and earnings growth as membership offers can drive user growth without the need for out sized increases to marketing spend.

Continued growth in membership numbers should only galvanize the loyalty the brand exhibits.

Financials & Valuations

Apologies for the quick calculations, however, I only had a short time to look at forecasts and the current price. Lulu has long been too rich for my blood and with a looming recession it appeared as if discretionary spend would suffer, dragging down the share price.

Whilst, I still expect a slowdown in retail spending, we cannot deny the strength the consumer has showed and also the quality of Lulu as a business. Therefore, I do think current prices represent an attractive entry for a starter position.

Please note I have combined historical figures with forecasted, sourced from Koyfin and any deeper slowdown in spending or US growth would likely see these numbers revised.

At the current price of $357, LULU 0.00%↑ is trading at a Forward P/E of 25x and PEG ratio of just above 1, figures it hasn’t traded at for some time. With a historical average P/E of 43x, there is significant room for return should the company simply meet the forecasted estimates. Growth in international revenues, product mix or through membership all provide optionality to exceed these levels contributing to a stronger return.

Whilst we may not see a return to growth in the upcoming quarter, the long-term trend for the business appears in-tact and therefore purchasing at these levels seems unlikely to result in a terrible return should you assume a 5 year holding period.

lululemon P/E history from full:ratio

Share price sensitivity table, using P/E multiples and forecasted EPS

Even when considering conservative figures from Koyfin, which do not account for any potential upside, projecting a 35x Price/Earnings ratio for Lululemon in 2027 would value the company at $632, resulting in favorable returns. If we assume the company trends towards a mature multiple of 25x, there is still potential for a decent return.

While I will outline risks below, it's important to note that impending rate cuts may also stimulate discretionary spending and bolster the equity markets in the medium term.

Risks

Slowdown in retail spending

A broader slowdown in retail spending, or a sharp increase in unemployment would hurt the near-term numbers for Lulu and likely drive the price lower. I would still assign this a fairly reasonable probability.

Broader Credit Event

The potential for a broader US credit event still exists, with a variety of CRE and Regional banking issues that may surface and halt the progress of the US economy, in this case I think it likely that discretionary spending equities suffer a sharp decline.

Resurgence in Inflation

The economy, in my opinion remains incredibly hot, and the high fiscal deficits, coupled with rising commodity prices I believe may result in a second surge in Inflation. In this case, the need for higher rates would weigh on Lululemon stock and broader US equities.

Apologies for the shallow analysis, please conduct additional research if this is something that may interest you.

Enjoy your day,

Disclosure: I am looking to purchase a position in Lululemon today. This blog is merely to document investment ideas and commentary and it is not meant to be financial advice. Please conduct your own research on all investments.

Sources:

Lululemon Athletica Q4 2023 Results, Lululemon Athletica Investor Relations, https://corporate.lululemon.com/investors/news-and-events/events-and-presentations/2023/lululemon-athletica-q4-2023-results, 08/04/2024

Lululemon Athletica P/E, full:ratio, https://fullratio.com/stocks/nasdaq-lulu/pe-ratio, 08/04/2024

Charts: Koyfin (1), Gurufocus (2), full:ratio (3)