Watchlist: Madison Square Garden Entertainment ($MSGE)

Watchlist: Madison Square Garden Entertainment ($MSGE)

Own a part of the NY skyline

Ticker: MSGE (Madison Square Garden Entertainment)

Market Cap: 1.85B

S/O: 48.3M

Thesis

Owner of the premier entertainment assets in New York City, irreplaceable venues and brand IP

Buffett-style investment - durable and long-lasting

Highly cash-generative assets and stable revenues from long-term licensing agreements

Renewed focus on returning capital to shareholders

Maintenance capex requirements only in near-term and minimal tax-payer through to 2026

Free call option on renovation of Penn St Station

Catalyst

While I view MSGE as having the potential for a long-term portfolio hold, a potential near-term catalyst exists in the location of the MSG Theatre. Please note, as of current there is no concrete plans and management has not made any clear indications of negotiation.

New York City is considering plans to modernize Penn Station, which may entail requesting MSG to sell the MSG Theatre and potentially grant access to a service road for construction purposes. Such a transaction could fetch approximately $500 million, representing roughly 20% of the company's market capitalization after taxes. Management has signaled their intention to return capital to shareholders, and this development could significantly impact the investment.

1. Background

I considered delving into the Dolan family's background, but let's skip that part as it might not be the most riveting read. Instead, let's dive straight into the spin and I suggest potential investors to quickly Google the family's history on Wikipedia if interested.

Madison Square Garden Entertainment (MSGE) & Sphere Entertainment (SPHR)

James Dolan (CEO and Chairman) and the management team at MSG believed that the best approach to maximizing the value of the various businesses under the MSG group umbrella was by spinning out the fast growing Sphere business, Tao Hospitality Group, and MSG Networks from the remaining mature entertainment venues located in New York City.

Sphere, known for its cutting-edge live events in Las Vegas, including a highly praised residency by U2, has captured significant attention for its immersive experiences. Dolan's enthusiasm for the potential of MSG Sphere is evident, especially considering discussions about constructing a second Sphere in London, although plans were halted due to concerns about light pollution—an issue worth exploring further.

Joining Sphere in the spin-off is Tao Group Hospitality, a renowned culinary and entertainment enterprise boasting over 80 locations featuring well-known brands. The final component is MSG Networks, a media and streaming company catering to the New York metro area with live coverage of local sporting events and expanded content including college football and basketball. This year, MSG Networks launched MSG+, a direct-to-consumer streaming service, and announced Gotham Advanced Media, a streaming joint venture aimed at enhancing fan engagement.

After looking in depth at Paramount, and gaining a greater understanding of the challenges in the direct-to-consumer streaming market, it wouldn't be surprising if Dolan considers divesting or selling MSG Networks. The competitive landscape in content creation across platforms has intensified, leading to increased merger and acquisition activity as firms seek consolidation to bolster offerings.

Dolan's appears bullish on the opportunity for Sphere, as is evident from his recent insider transactions of Sphere and sales in MSGE, whilst this may have occurred for any number of reasons we must consider it a signal on Dolan's confidence in there Sphere operating model. Where Sphere can generate revenue from its primary source, concerts and entertainment, the large display exterior can also be used to generate advertising revenue even whilst it stands dormant. Something that cannot be said for the traditional venue.

There is strong momentum behind the Sphere business, with Las Vegas growing at an exponential rate and more large-scale entertainment events than ever before (NFL, NHL, F1), However, I think concerns around light pollution remain valid, and whilst we may see additional Sphere's pop up in spend-happy countries like the middle-east, I believe many cities will be forced to consider the light pollution from a venue that emits 24-7, just as London has.

Nonetheless, what remains within the SpinCo, MSGE, comprises a portfolio of world-class entertainment assets poised to capitalize on the resurgence of interest in live entertainment. With a management strategy that now has the flexibility to focus on unlocking shareholder value, MSGE stands as an attractive investment opportunity. So let's go over the assets.

2. Assets Overview

Madison Square Garden

Madison Square Garden, the number 1 grossing venue of its size globally and affectionately known as 'The World's Most Famous Arena,' has stood as a symbol of cultural and historical significance since its construction in 1879.

Serving as the home to iconic sports teams like the New York Knicks and Rangers, the venue boasts a seating capacity of 21,000. Over the years, it has undergone numerous renovations, with the most recent significant upgrade completed in 2013. This transformative renovation expanded its capabilities to host a wider array of events, with enhanced hospitality amenities and increased capacity for entertainment, solidifying its position as a premier destination for unforgettable experiences.

With such heritage the venue is one of the first options for corporate hospitality packages and demand is in no shortage located in Lower Manhattan and in close distance to Wall St. The Garden is special to everyone for so many reasons; some key historical events include;

1970 Knicks Championship & 1994 Rangers Stanley Cup

1971 "Fight of the Century" between Muhammad Ali and Joe Frazier

Marilyn Monroe serenading John F Kennedy for his birthday

And my personal favourite, Kobe Bryant going off for 61 points against the Knicks, for the then stadium record.

Theatre at Madison Square Garden

The Theatre is located within the MSG complex and offers a smaller and more intimate setting compared to its larger counterpart. With a seating capacity of up to 5,600, it has played host to an impressive lineup of legendary artists such as Elton John, Stevie Wonder, and Bob Dylan. Additionally, the Theatre has become a hot-spot for comedy, with acclaimed comedians like Dave Chappelle, Kevin Hart, and others gracing its stage

Commentary has arisen of late regarding New York's Penn Station. It is dire need of renovation and there is rumours circling that MSGE may in fact be asked to divest the Theatre to allow for such improvements, whilst it remains conjecture for the time being, prices have been floated in the region of $500m, or 25% of the current market cap of $1.85B.

Radio City Music Hall

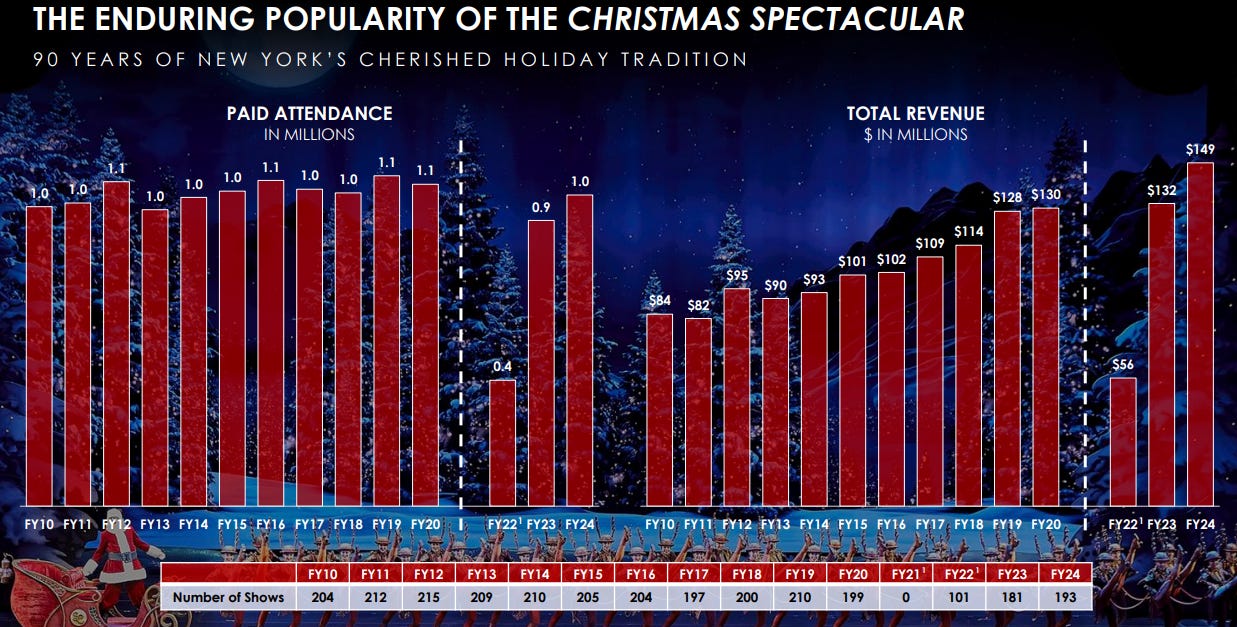

Radio City Music Hall stands as an iconic entertainment venue in the heart of New York City, celebrated as a cultural landmark and revered for its stunning architecture and lavish design. Since its opening in 1932, it has become synonymous with the spirit of New York. The venue is famously home to the Radio City Rockettes, who have been entertaining audiences for nearly a century, since their formation in 1925. The Rockettes are a key feature of the annual Christmas Spectacular, a renowned holiday production that showcases elaborate costumes, festive music, and Christmas magic.

The Christmas Spectacular has been delighting audiences for over 90 years and despite its long history, it continues to attract significant interest, with MSGE increasing the number of shows this past Christmas due to heightened demand. MSGE management believes that both the Christmas Spectacular and the Rockettes hold significant potential for expansion through improved media and marketing strategies

Note the venue is not owned by MSGE but is leased through to 2038

Beacon Theatre

The Beacon Theatre is another iconic New York venue, located in the Upper East side of Manhattan. Built in 1929, the Beacon is known for its incredible art-deco design and is another cultural landmark of the city. Venue capacity can reach 2,800 and has seen many legendary performers throughout the years.

Note the venue is not owned by MSGE but is leased through to 2036

Chicago Theatre

Finally, we arrive at the last venue the Chicago theatre, another landmark venue, located in downtown Chicago, the theatre has and continues to be a cultural hub for entertainment. The Chicago venue was built in 1921 and can seat up to 3,600.

3. Irreplaceable - Brand & IP

Sports Licensing

We've explored the tangible assets contributing to MSG revenues, but delving into the intangible value of the company's intellectual property (IP) is essential to grasp the true worth of the business.

New York boasts some of the world's most fervent sports fans, and MSG holds enduring access to two iconic global sporting franchises: the New York Knicks and Rangers. With agreements secured until 2055, licensing payments generated $42 million in revenues for FY 2023, projected to grow steadily at 3% throughout the agreement period. Furthermore, MSGE benefits from additional revenue streams, including profit-sharing arrangements with sponsors, merchandise sales, and related activities.

(Note, that the timing of events in the reporting period for both Rangers and Knicks can have a short term effect on revenues causing some short-term reporting volatility)

Christmas Spectacular and the Radio City Rockettes

New York City has long-held the reputation as one of, if not the, world's premier city, holding over 23 million residents and attracting a staggering 65 million visitors annually. Renowned as the epicenter of commerce, it hosts the highest number of Fortune 500 companies and is acclaimed as the number one concert and entertainment market globally. It is this vibrant landscape that consistently lures top talent to its entertainment venues and creates an increased stability to revenues that would otherwise be considered highly discretionary.

The Christmas Spectacular, marking its 90th year of production, continues to demonstrate enduring popularity, as depicted in the graphic above. Although revenue experienced a slowdown in 2020 due to challenges in travel and hospitality, signs of recovery are evident. Heading into the end of 2023, demand surged, prompting management to add additional shows, totaling 193 for the year compared to 183 the prior year.

The increased volume of shows, coupled with higher pricing, resulted in a remarkable 30% increase in average per-show revenue year-over-year, surpassing pre-COVID levels by 10%. While some moderation may be expected, the stability of interest indicates a promising outlook.

Central to the Christmas Spectacular is the iconic group, the Radio City Rockettes. With their performances traditionally centered around the holiday period, management sees significant potential for expansion, particularly given their burgeoning online presence.

Looking ahead, management perceives a broad opportunity for growth within the Christmas Spectacular franchise, benefiting from stable demand and limited marketing needs. Additionally, leveraging the growing presence of the Rockettes presents further revenue opportunities through brand development, marketing initiatives, and sponsorship.

Success is driven by the Artist-first approach

A cornerstone of MSGE's business model lies in its ability to cultivate lasting relationships with artists throughout their career journeys. With four premier venues in New York City, ranging from the intimate 3,800-seat Beacon Theatre to the grandeur of Radio City Music Hall (6,000 seats) and Madison Square Garden (over 21,000 seats), the company offers a seamless platform to support artists' evolving needs. These strong artist relationships are pivotal in securing top-tier entertainment bookings.

Moreover, the challenges posed by the COVID-19 pandemic have resulted in a buildup of artists eager to tour and perform in the coming years. This positions MSGE favorably to capitalize on the anticipated surge in live entertainment demand. With its strategic presence in four key entertainment venues within one of the world's largest cities, MSGE commands a near-monopoly in the New York entertainment market, further solidifying its dominant position.

"We expect to benefit in future years from continued industry growth as an increasing number of artists and acts continue to go on tour.” - MSGE Management

4. Capital Allocation & Structure

I should have addressed this earlier, but I want to emphasize the new post-spin capital structure, the voting rights of the company, and the capital allocation policy of management moving forward, as I believe this last point is a crucial aspect of the MSGE investment thesis.

Regarding how the strategy may change now that the company has been spun, I believe it's best to directly quote management rather than provide my own interpretation, rather than detail myself.

“We're primarily focused on driving organic growth across our operations. Driving growth in per event revenues and profitability, increasing utilization at the venues, expanding our corporate partnerships businesses, maximizing revenue and profit for the Christmas Spectacular, and yes, we will also continue to look for ways to operate more efficiently, more effective marketing initiatives to how we operate the Christmas Spectacular for example. One thing that has changed as a result of the spin though is, we now have the flexibility as a standalone company to pursue a capital allocation strategy that's appropriate for the business.”

What stands out is flexibility, MSGE holds a portfolio of highly cash-generative, mature assets, with a direct focus on improving operations and returning value to shareholders, I believe this can be a stable and rewarding long-term investment.

Management has outlined a clear strategy for the coming years, emphasizing debt reduction and the opportunistic return of capital to shareholders. Progress has already been made in addressing liabilities, and while debt levels remain elevated, management expresses confidence in swiftly deleveraging as Adjusted Operating Income (AOI) increases and the noise from post-spin adjustments to operating income dissipates.

It is worth noting that Sphere Entertainment retained approximately 33% of the outstanding shares of MSGE. Instead of allowing an extended sale of these shares in the market, management opted to engage with Sphere and repurchase shares directly. A portion of these repurchases were funded through an announced $250 million share repurchase program, of which $110 million remains. To date, approximately 10% of outstanding shares have been repurchased since the spin-off. Furthermore, management has shown a willingness to utilize the company's revolving credit facility for share repurchases opportunistically

I believe this renewed focus is promising for potential shareholders, management appears focused on driving operational efficiency in the current business assets, and has highlighted there is minimal capex expected for the foreseeable future, with near-term capex being largely maintenance driven. There are no current plans to perform any significant renovations on the venues, and there are no plans to engage in any M&A. The goal remains clear on driving performance and rewarding shareholders where possible.

A final point on voting rights, MSGE holds two share classes, A & B. Classes receive the same dividend rights, however, Class B shares held by Dolan control the majority of voting rights. I don’t see this having any detrimental effect to shareholders.

5. Revenues & Upside

As illustrated in the graphic above, MSGE is able to generate revenues from a well-diversified revenue base and is not reliant on any one stream. The source of revenues, whether licensing from Sports, consistency of the Christmas Spectacular or the long-term agreements for sponsorship and suites provide a stable base of revenues that will allow the company to generate significant free cashflow in the coming years.

There are 5 key factors I would like to highlight on how the company generates revenues but also where I believe there is potential upside for future operational efficiency gains. I will detail a variety of opportunities in the below, however, where management believes the greatest potential lies, is in increased venue utilization and driving higher per-event revenues.

Tickets

As we emerge from the challenges of the COVID-19 pandemic, sales have shown a notable uptick, a trend further evidenced by the US Consumer Price Index (CPI) reports, reflecting the resilience of the US consumer. While we touched on management’s ability to successfully expand productions like the Christmas Spectacular by adding additional shows, the focus moving forward lies in enhancing the pricing strategy for ticket inventory.

By improving their dynamic pricing for ticket inventory, management is aiming to reduce ticket discounting and incrementally boost ticket yield in periods of strong demand. This approach not only improves revenue per ticket but also allows for additional earnings to flow directly to the bottom line, as it leverages off a stable cost base. These measures should position the company to improve profitability and continue to capitalize on the rebounding consumer demand.

Hospitality Packages

At the core of the MSGE brand are its exceptional hospitality offerings. As previously mentioned, each venue holds significant cultural importance and exudes a sense of sophistication. While I won't delve into each individual offering, MSGE boasts over 100 premium hospitality options, ranging from suites to lounges, catering to a diverse range of events.

Thus far, the Premium Hospitality offerings have garnered exceptional reception, with the majority of suites operating under long-term agreements featuring annual pricing escalators. Activity levels have surpassed pre-COVID levels, and this year, management successfully introduced two new suites at MSG. A multi-year agreement has already been secured for the event suite, while the luxury event level club is nearing full occupancy. Demand for these offerings remains remarkably robust.

Licensing

I have touched on Licensing above, so I won’t detail too much further, however, long term agreements are in place with MSG Sports (Knicks and Rangers). These long-term agreements feature annual price escalators of 3%, providing a stable revenue base. Additionally, the company benefits from ticket sales, merchandise, and sponsorship associated with these teams.

Strong team performances and additional games can directly translate into higher revenues for the company, further bolstering our financial outlook

Bookings & Venue Utilization

With the a large portion of revenues being derived from physical venues, the company faces limitations on the number of events it can host due to the finite number of days in a year. Therefore, to enhance efficiency and drive revenue, the focus must shift towards optimizing metrics such as maximizing venue utilization and increasing bookings to improve per-event revenue. This strategic focus is paramount for management moving forward, although it's worth noting their strong track record in growing annual events.

Following the transformation of Madison Square Garden (2013-2015), the company has achieved mid-single-digit growth in events across all venues. However, since Madison Square Garden is the largest venue, it holds the greatest potential upside if the company can improve its utilization.

Historically, MSG operates at approximately 70% utilization, equating to around 230 events annually out of 365 days. Some days are lost due to logistical requirements such as load-in/load-out, necessitating venue adjustments for upcoming events.

Management is exploring various strategies to enhance utilization, including scheduling multiple events per day (day/night) and increasing the number of artist residencies. As previously mentioned, the success of Sphere's 40-night U2 concert series underscores the viability of such approaches, which not only meet strong demand but also reduced the need for continued stage set alterations.

This aspect will be pivotal to the investments thesis and will be closely monitored moving forward..

Sponsorship, Marketing, Advertising

Sponsorship, marketing, and advertising play significant roles in sports and entertainment branding. MSG boasts such a strong presence in the New York entertainment community that it has attracted major sponsorship partners, contributing to revenue growth. Partnerships with companies like Verizon, Spectrum, HUB Group, and QVC provide substantial revenue, albeit with potential for periodic fluctuations due to renewal cycles, typically occurring every few years.

Management believe there is significant upside potential in sponsorship opportunities and sees variety of emerging verticals they believe they can capture moving forward, where they were able to do something similar with the introduction of sports betting to the NY.

It is worth noting that recently MSGE announced an agreement with Oak View Group, which is a global stadium development and investment company. They have a dedicated sponsorship team for sports entertainment and MSGE management believe that utilizing their services and moving to a more variable commission style model for sponsorship will benefit the company moving forward.

6. Financials/Debt

Apologies for the disjointed financials. As the company continues to work through adjustments and restructuring costs, we will still require additional quarterly data to gain a more consistent understanding of the movements in the financial statements.

However, based on the available information, it's evident that the fourth quarter, (Christmas quarter) will account for the lion’s share of the yearly revenues. This is largely attributed to the Christmas Spectacular, which significantly contributes to both revenues and operating income during the period. Restructuring charges associated with termination of employees and the transfer of share-based compensation costs are still skewing the true operating numbers of the company. We should also mention a fairly turbulent financial history due to covid lock downs.

In FY23, the company achieved revenues of $850 million, with expectations for FY24 revenues in the range of $930 million to $950 million. If we consider the midpoint, we anticipate a growth rate of 10-12%. Adjusted Operating Income (AOI) for FY23 was initially forecasted at $155 million but surpassed expectations, reaching $175 million. For FY24, AOI is forecasted to range between $170 million and $180 million, with Q2 already generating $150 million, suggesting the potential for this figure to exceed $180 million.

The company's free cash flow yield has averaged 12%, and 8% on an after-tax basis. This metric is expected to improve as the company continues to enhance operations and implement pricing strategies

Reviewing the debt schedule outlined above, it's apparent that the principal repayment is heavily weighted toward the later years, with maturity in 2027. I anticipate the likelihood of this being extended further over time. Management has projected interest payments in the range of $45 million to $50 million, which while not insignificant, are well within the company's capacity to manage given its robust cash flow generation. Additionally, the availability of a revolving credit facility offers further flexibility.

Although management has not established a specific target leverage level, they anticipate that deleveraging will occur naturally over the coming years. With minimal expected capital expenditure and the company's projection of being a minimal taxpayer through to 2026, there exists ample opportunity for capital return to shareholders

7. Valuation

I won’t delve into the details of the macro environment, but it's worth noting that current market conditions have driven stocks higher for the past five months. By rough calculations, MSGE is trading at 15x-18x 2024 Free Cash Flow (FCF), potentially facing some near-term headwinds in consumer demand if there's a broader slowdown in US retail spending.

However, I firmly believe that the long-term trends for live entertainment remain intact, and MSGE boasts premier entertainment assets in the world's greatest city. With a focused and targeted approach, management should be able to generate significant free cash flow in the years ahead, facilitating share repurchases, debt reduction, and potentially even the initiation of a dividend. Shareholders also benefit from a free call option on the Penn Station renovation, which could significantly enhance capital returns.

In a nutshell, I view MSGE as a Buffett-style investment, with assets that are likely to endure. While I'm not looking to enter at current levels, I'll continue to monitor the company and may consider accumulating shares for the long term if and when the price becomes more favorable.

I hope you found this insightful and encourage you to explore MSGE further.

Disclosure: I do not hold MSGE, but may do so in the future. This blog is merely to document investment ideas and commentary and it is not meant to be financial advice. Please conduct your own research on all investments.

Source:

Madison Square Garden Entertainment. (2023, February 16). MSGE SpinCo Investor Presentation.

Madison Square Garden Entertainment. (2024, February 7). 2Q 24 Investor Presentation.

Madison Square Garden Entertainment. (2024, February 7), Financial Statements

Arch Paper - https://www.archpaper.com/2023/11/the-three-railroads-operating-out-of-penn-station-prioritize-performance-in-plans-to-redesign-the-transit-hub/